Your Guide to the Secretary of State Annual Report

- Read & Associates

- Feb 13

- 15 min read

A secretary of state annual report is a mandatory filing that keeps your U.S. company’s information current with the state where it's registered. Don't let the name intimidate you. Think of it less as a complex financial document and more as a routine 'check-in' to confirm your business is still active and compliant. It’s a simple but critical task for keeping your company in good legal health.

Demystifying the Annual Report Requirement

For many UK founders, the term "annual report" probably brings to mind hefty financial audits or complicated tax returns. Let's clear that up right away. In this context, a Secretary of State annual report is much simpler—it's essentially your company's yearly subscription renewal to operate legally in a particular state.

Its main purpose is to ensure the state has accurate, up-to-date public information about your business. This isn't about your revenue, profits, or losses. It's simply a chance to verify your company’s core operational details.

What Information Is Typically Required?

While the specifics can vary a bit from state to state, most annual reports just ask you to confirm or update the fundamental information you provided when you first registered. It’s a chance to note anything that has changed over the past year.

You'll usually be asked for:

Official Company Name: Just confirming your legal business name is still the same.

Principal Business Address: Your main U.S. business location, which for most UK founders is a virtual address.

Registered Agent Details: Confirming the name and address of your designated U.S. contact for official mail. If you want a refresher, you can learn more about what a registered agent is and why your U.S. business needs one in our detailed guide.

Names and Addresses of Directors/Members: Listing the key people managing the company.

This process ensures total transparency, allowing the public, other businesses, and government agencies to access current, reliable information about your entity.

The core function of the Secretary of State annual report is compliance, not accounting. It's designed to keep your business in 'good standing'—a status that proves your company is legally registered and has met its basic state obligations.

Why "Good Standing" Matters So Much

Maintaining "good standing" isn't just about ticking a bureaucratic box; it’s the key that unlocks crucial business functions in the U.S. Without it, your company can hit some serious roadblocks.

Being in good standing is often a non-negotiable requirement for:

Opening a U.S. business bank account: Banks will check your company’s status before they even consider your application.

Securing loans or funding: No lender or investor will touch a company that isn't legally compliant.

Entering into contracts: Potential partners will verify your status to make sure they're dealing with a legitimate, active company.

Protecting your personal liability: For LLCs and corporations, good standing helps maintain the "corporate veil" that separates your personal assets from business debts.

Failing to file this straightforward report can put your company’s good standing at risk, leading to penalties and, in a worst-case scenario, administrative dissolution by the state. This makes the annual report a small but powerful tool for protecting your entire U.S. venture.

Decoding State-by-State Filing Differences

One of the biggest culture shocks for UK founders setting up a US company is discovering there's no single, federal rulebook for business compliance. The secretary of state annual report is the perfect example of this. Think of the US not as one country, but as 50 different regulatory environments, each with its own set of rules, deadlines, and fees.

This patchwork system means you can't use a one-size-fits-all approach. A deadline that works for your friend's company in Florida will be completely wrong for your LLC in Delaware. This is precisely why staying organised and understanding the specific rules for your state is non-negotiable for keeping your company in good standing.

Key Differences You Will Encounter

For a non-resident founder, getting a handle on these variations is the first step to successful compliance. While the basic idea of the report is always the same—updating the state on your company's core details—how you actually do it can differ wildly.

Here’s where things get tricky from state to state:

Filing Deadlines: Some states set a universal deadline for every business, like Florida’s May 1st cut-off. Others tie it directly to the anniversary month of your company’s formation, which requires a more personalised calendar.

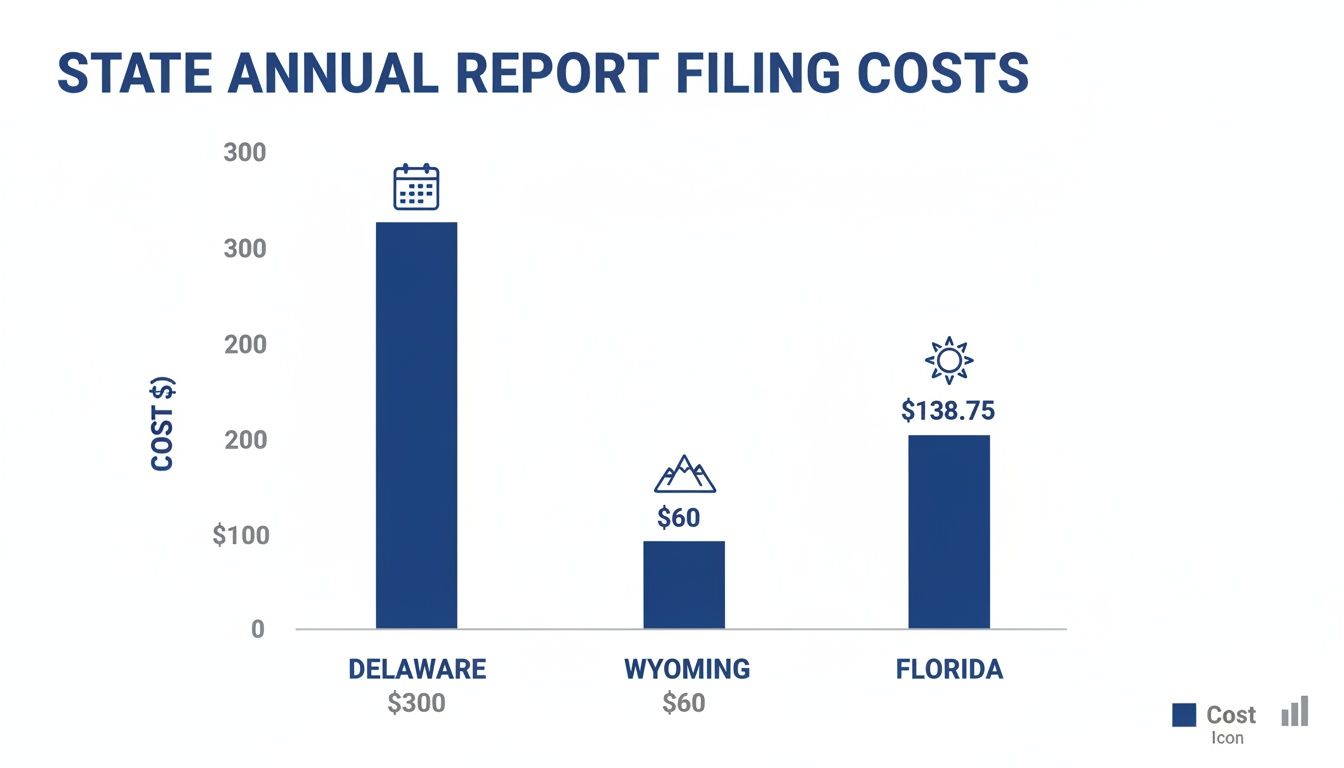

Filing Fees: The costs are all over the map. You might pay as little as $60 in a business-friendly state like Wyoming, but face hundreds of dollars elsewhere. Delaware, for instance, has a franchise tax system for corporations that can push the cost up significantly.

Report Terminology: Even the name of the report changes. In Florida, it’s an "Annual Report," but head over to California and it’s a "Statement of Information." In Texas, they call it a "Public Information Report." They all accomplish the same goal, but you need to know what to look for.

These state-level quirks are only getting more important as federal oversight grows. The U.S. Department of State’s FY 2025 Agency Financial Report signals a broader push for financial transparency, and that sentiment is trickling down to the states. With over 50 states and territories requiring these filings—at an average cost of $100 to $800 a year—getting it right has never been more critical, especially with new federal rules like the Corporate Transparency Act in play. You can get a sense of the government's direction by reviewing the full agency financial report findings.

Comparing Popular States for UK Founders

To see just how different things can be, let’s look at three states that are popular hotspots for international founders: Delaware, Wyoming, and Florida. Each offers great benefits, but their reporting rules couldn't be more different. Wyoming, for instance, is famous for its simplicity and low fees, which is why we see so many UK founders flock there. For a closer look at what makes it so attractive, check out our guide on forming an LLC in Wyoming for UK founders.

Putting them side-by-side really highlights why you can't make assumptions.

Key Takeaway: Never assume the rules from one state apply to another. Always verify the specific requirements for each state where your company is registered to avoid accidental non-compliance.

The table below breaks down the must-know details for LLCs in these key states, giving you a clear snapshot of what to expect.

Annual Report Filing Requirements in Popular States for UK Founders

This table compares the essential annual report details for LLCs in states commonly chosen by international entrepreneurs. It clearly illustrates the dramatic differences in deadlines, costs, and penalties you'll encounter.

State | Typical Due Date | Average Filing Fee | Key Information Required | Late Filing Penalty Example |

|---|---|---|---|---|

Delaware | June 1st (for LLCs) | $300 (Flat Tax) | Registered Agent Name & Address | $200 Penalty + 1.5% Monthly Interest |

Wyoming | First day of anniversary month | $60 | Principal Office & Mailing Address | Administrative Dissolution after 60 days |

Florida | May 1st | $138.75 | Principal Address, Registered Agent, Member/Manager Info | $400 (Cannot be waived) |

As you can see, the consequences of a simple mistake vary enormously. A UK founder with a Florida LLC who misses the May 1st deadline is hit with a hefty, non-negotiable $400 late fee. Meanwhile, a founder with a Wyoming LLC has to file by their company's anniversary month to avoid a much smaller fee but faces a far more serious threat: the state could dissolve their company after just 60 days.

These stark differences drive home the need for a state-specific compliance strategy. Without one, you're not just risking a fine; you're putting your entire US business operation in jeopardy.

The High Cost of Missing Your Filing Deadline

Think of your secretary of state annual report as the legal pulse of your U.S. company. Forgetting to file it isn't just a minor administrative slip-up; it's like letting your company's registration expire, and the fallout can be swift and severe. This one mistake can set off a chain reaction of problems that could seriously threaten your entire U.S. venture. If you're running things from the UK, cleaning up the mess from overseas is a whole other level of headache and expense.

The first hit is always to your wallet. States don't mess around with late fees. In Florida, for example, miss the May 1st deadline and you're immediately hit with a stiff $400 penalty. No excuses. Over in Delaware, you're looking at a $200 late fee plus 1.5% interest tacked on every month—not just on the fee, but on the original tax amount, too. These fines are meant to hurt, pushing you to stay compliant and quickly turning a simple task into a major cost.

The initial filing fees themselves vary wildly, which just magnifies the impact of any late penalties.

As you can see, the starting line is different everywhere, from Wyoming's manageable $60 to Delaware's $300 flat tax. That's why having a state-specific budget is so important. For a deeper dive, check out our guide on the real cost to form an LLC for UK founders.

Losing Your Good Standing

Beyond the fines, your company's status will be downgraded, and it will lose its "good standing" with the state. This isn't just some bureaucratic label; it's the state's official seal of approval that you're operating legally. Without it, your company is essentially locked out of doing business.

When your company isn't in good standing, you’ll suddenly find you can't:

Access U.S. Banking: Banks might freeze your accounts or refuse to open new ones until you're back in compliance.

Secure Loans or Investment: No investor or lender is going to touch a company that isn't legally sound.

Enforce Legal Contracts: You could lose the right to sue another business in that state's courts, making your contracts unenforceable.

Renew Business Licenses: Any state-level permits or licenses you need to operate will be impossible to renew.

For a founder in the UK, this can bring your U.S. operations to a grinding halt, making it impossible to pay your team, get paid by customers, or move the business forward.

The Danger of Piercing the Corporate Veil

Here’s where things get really serious. One of the biggest legal risks of non-compliance is known as "piercing the corporate veil." This is a legal doctrine where a court ignores the liability protection of your LLC or corporation and holds you, the owner, personally responsible for the company’s debts and lawsuits.

Your LLC is supposed to be a shield, creating a wall between your personal assets (your home, your savings) and your business liabilities. Failing to file your annual report is like putting a crack in that shield. If your company gets sued, the other side can argue you didn't treat the company as a separate legal entity, leaving your personal assets totally exposed.

The Ultimate Penalty: Administrative Dissolution

If you ignore the warnings and let the penalties pile up—often for just 60 to 120 days—the state will drop the hammer: administrative dissolution. This means the Secretary of State officially terminates your company's existence. It’s gone. Your business name is back up for grabs, and your entity is legally dead.

Trying to reverse an administrative dissolution is a nightmare. The process, called reinstatement, requires you to pay all the back taxes, late fees, and interest you owe, plus hefty reinstatement fees. While you’re sorting that out, any business you conducted or contracts you signed while dissolved could be declared invalid. It’s a massive legal and financial mess that's incredibly stressful to fix, especially from another country.

A Practical Filing Checklist for UK Founders

Running a U.S. business from the other side of the Atlantic comes with its own set of hurdles. When it comes to your secretary of state annual report, a little prep work can make the difference between a smooth filing and a major headache.

This isn’t just about dodging a last-minute scramble. It’s about getting the details right to prevent bigger problems down the road. Use this pre-flight checklist to get all your ducks in a row before you even think about logging into a state portal.

Your Pre-Filing Essentials

Before you start, run through these five critical checks. Having this information confirmed and ready to go will turn a potentially confusing task into a straightforward one.

Confirm Your EIN Is Correct: Your Employer Identification Number (EIN) is your company’s tax ID in the States. Double-check that you have the right number from your original IRS confirmation letter (the CP 575). A simple typo here can get your entire filing rejected.

Verify Your Registered Agent Details: Your registered agent is your official point of contact on U.S. soil. You need to confirm their name and physical address are up-to-date in the state's records. If you've recently switched providers, make sure the state knows about it.

Check Your U.S. Business Address: Make sure your U.S. virtual address is active and can still receive mail. This address is on the public record, so accuracy is non-negotiable.

Gather Officer and Member Information: Have the full legal names and current business addresses for every company member (for an LLC) or all officers and directors (for a corporation). States require this to keep a clear record of who is running the show.

Identify Your State Filing Number: Every state gives your company a unique ID number—it might be called a UBI number, file number, or entity number. You’ll need this to look up your company on the state’s filing system, so find it and keep it handy.

Treat this checklist like an annual health check for your company's core data. A small error in a registered agent's address or an outdated officer list can create compliance headaches that are much harder to solve from overseas.

Navigating Multi-State Filing Obligations

For many UK founders, especially in e-commerce, your compliance duties don't stop in the state where you formed your company. If your business has a significant presence—what's known as "nexus"—in other states, you probably have filing obligations there, too.

A classic mistake is thinking that filing your annual report in Delaware or Wyoming covers you everywhere. It doesn't. If you've officially registered to do business in another state (a process called foreign qualification), you absolutely must file an annual report and pay the fees there as well.

This has become a huge deal for UK startups since the 2018 Supreme Court decision in South Dakota v. Wayfair. That ruling established that significant economic activity, not just a physical office, can create nexus. Now, e-commerce sellers often have to deal with sales tax in over 45 states, triggered by hitting thresholds like $100,000 in sales or 200 transactions. This new landscape underscores why you have to understand your company's complete U.S. footprint. You can learn more about how U.S. regulations impact foreign businesses and explore investment protections in Treasury reports.

Key Questions for Multi-State Nexus

Not sure if you have other filing duties? Ask yourself these questions:

Have we registered in other states? If you’ve foreign qualified your LLC or corporation anywhere, you have a direct filing requirement there. End of story.

Do we have employees in other states? Hiring U.S. staff outside your home state almost always creates nexus.

Do we store inventory in other states? If you use a service like Amazon FBA, your products are sitting in warehouses across the country. That creates nexus in those locations.

If you answered yes to any of these, you likely have more than one annual report to file. Staying on top of these multi-state requirements is crucial for keeping your entire U.S. operation compliant and in good standing.

How Set Up Stateside Makes Your Compliance Effortless

Let's be honest. Juggling different deadlines, fees, and quirky state portals for your secretary of state annual report is a nightmare, especially when you're an ocean away. That kind of administrative drain sucks up time and focus—two things you absolutely can't spare when you're growing a business. This is exactly why having a dedicated compliance partner isn't a luxury; it's a necessity.

At Set Up Stateside, we’ve designed our entire service around turning this annual chore into a simple, hands-off process. We don't just ping you with reminders. We take the whole thing off your desk so you can get back to what you do best: building your company, innovating, and taking care of your customers.

Proactive Management Across All 50 States

For UK founders, the biggest compliance risk is often the one you don't see coming. A missed deadline in a state where you have a minor presence can still trigger penalties or even cost you your good standing. We're here to make sure that never happens.

Our system is built to track your obligations in every single state you're registered in. We’re not just watching your primary state of incorporation; we're managing your entire U.S. operational footprint.

Meticulous Paperwork Preparation: We gather the right information and prepare every report with an obsessive eye for detail. Accuracy is everything.

Complete Submission Management: Our team takes it from there, navigating each state’s unique online portal or mail-in process from start to finish.

Confirmation and Record-Keeping: Once a report is filed, we send you the official confirmation and keep meticulous records, giving you a clean, clear paper trail for your business.

It’s a truly hands-off approach. Your company stays compliant everywhere, all the time, and you never have to wrestle with a clunky government website again.

An Integrated System for Total Peace of Mind

Real compliance isn't just about filing a single report on time. It’s about building a system where all the administrative pieces of your U.S. operation fit together perfectly. That’s why we bundle our services to create a complete support structure designed specifically for founders like you.

When you work with us, you get much more than just report filing. Our integrated services cover all the bases:

Registered Agent Service: We serve as your official point of contact in the U.S., ready to receive and process any legal notices or state mail right away.

U.S. Business Address: You get a stable, professional U.S. address for all your official correspondence, giving you a reliable home base.

Expert Bookkeeping: Clean books are the bedrock of good compliance. Our accounting team makes sure your financials are always accurate and up-to-date.

By combining these essentials, we give you a single, reliable system for managing your U.S. company. You get one dedicated partner, one point of contact, and one team making sure every single compliance box is ticked.

Securing Your Scalability and Future Growth

Staying on top of your compliance is fundamental to building a scalable business. It keeps you eligible for new opportunities and protects you from serious threats. Something as simple as a missed annual report can block you from securing funding, get your bank accounts frozen, or even lead to administrative dissolution—all of which can be devastating.

The good news is that the U.S. market is incredibly supportive of businesses that play by the rules. In fiscal year 2025, the U.S. Small Business Administration (SBA) guaranteed 85,000 loans totaling an incredible $45 billion. That kind of support is available to companies that maintain their legal and financial health, and our job is to make sure you're always in a position to benefit. You can find out more about the SBA's support for small businesses in their annual report.

With Set Up Stateside handling your annual reports and ongoing compliance, you get the most valuable asset of all: peace of mind. You can push for growth with confidence, knowing your U.S. venture is secure, compliant, and always ready for its next big move.

Your Annual Report Questions Answered

Even with the basics covered, a few practical questions always pop up when it's time to file. For UK founders managing a U.S. company from across the pond, these little points of confusion can feel like big hurdles. Let's tackle the most common head-scratchers we hear every day.

Think of this as your quick-reference guide for a dose of clarity and confidence.

Is This the Same as My Federal Tax Return?

This is easily the most frequent mix-up, so let’s clear it up right away: No, they are completely different. Your state annual report and your federal tax return are separate filings, for separate government agencies, with totally different purposes.

It helps to think of it like this: your state annual report is like renewing your company’s public business registration, while your federal tax return is a private report to the IRS about your finances.

State Annual Report: This is a public document filed with your state's Secretary of State office. It’s purely for administrative housekeeping—keeping your company’s contact and management info up-to-date. There is zero financial data on this report.

Federal Tax Return: This is a confidential financial document filed with the Internal Revenue Service (IRS). It's where you detail your company's revenue, profits, and losses to figure out how much tax you owe.

You have to file both to stay compliant. Missing one doesn't get you out of filing the other.

Do I Still Need to File If My Company Made No Money?

Yes, absolutely. Your duty to file the annual report has nothing to do with whether your company made a single dollar. Even if your LLC had $0 in sales and zero activity all year, you are still legally required to file that report and pay the fee.

The state sees your company as an active legal entity from the day it's formed until the day you formally dissolve it. The whole point of the annual report is simply to confirm your company still exists and its details are correct, regardless of its bank balance. Ignoring it because your business was dormant will land you in the exact same trouble—penalties, loss of good standing, and eventually, the state shutting your company down.

A classic rookie mistake is thinking "no business activity" means "no paperwork." In reality, your compliance clock starts ticking the second your company is approved and doesn't stop until you officially close up shop.

What If My Company Information Has Changed?

That’s exactly what the annual report is for! It's not just a box-ticking exercise; it's the designated time to update the state on any changes to your company’s core information. If your business address changed or you brought a new member on board, you just enter the new, correct info when you submit the report.

Common updates you can make directly on the report include:

Changing your principal business address

Updating your U.S. mailing address

Adding or removing members, managers, or directors

Updating the personal addresses for existing members or managers

Just be aware that bigger changes usually require a different form. For instance, to legally change your company’s name or appoint a new registered agent, you’ll likely need to file a separate "Article of Amendment" or "Change of Registered Agent" form. It's always a good idea to double-check your state's specific rules.

Where Do I Actually Go to File the Report?

Good news: you almost never have to deal with snail mail anymore. Nearly every state has an online portal that makes filing your annual report quick and painless.

You'll just need to head to the official Secretary of State website for the state where your company is registered. For example, if you're registered in Washington, you'd visit the Corporations & Charities Filing System on the WA Secretary of State’s site.

You’ll need your company’s unique state-issued ID number (sometimes called a UBI number) to look up your business and get started. From there, you just fill out the online form, pay the fee with a credit card, and get an instant confirmation. We always recommend filing online—it's faster, and you get immediate proof that you’ve done it.

Managing U.S. compliance from the UK shouldn't be a source of stress. Set Up Stateside provides a dedicated, hands-off service to manage all your annual report filings, ensuring you never miss a deadline or risk your company's good standing. Let us handle the details so you can focus on growth. Learn more about our compliance services today!

Comments