How to Prepare Financial Statements A Guide for UK Founders in the US

- Read & Associates

- Feb 15

- 17 min read

So, you're a UK founder with a US company. Now comes the fun part: the financials. To get your books in order, you'll need to pull together all your financial transactions for a specific period and then shape that data into three core reports: the Income Statement, the Balance Sheet, and the Statement of Cash Flows.

This isn't just about number-crunching. It's about translating your day-to-day bookkeeping into a clear story of your company's financial health. This story is crucial for staying compliant, keeping investors happy, and making smart business decisions. For founders coming from the UK, the most important thing to remember is that this entire process has to follow US Generally Accepted Accounting Principles (GAAP).

Your Essential Roadmap to US Financial Reporting

For a UK founder, diving into US financial reporting can feel like you're trying to learn a new language overnight. But trust me, getting this right is the bedrock of investor confidence and long-term growth. This guide is designed to break down the process, focusing on what you need to know and pointing out the key differences between UK and US accounting practices.

Why Accurate Statements Are Non-Negotiable

These reports aren't just bureaucratic box-ticking. They are absolutely essential for a few very important reasons. You can't file your federal or state taxes, open a US bank account, or even think about raising funds from US investors without them. They are the official, legal record of how your business is performing.

Everything starts with clean, accurate bookkeeping. According to a Thomson Reuters survey, over 75% of tax firms say business tax return prep—which relies entirely on good financial statements—is their most profitable service. Yet, nearly half (47%) of those same professionals admit that a lack of time and resources is their biggest roadblock. That tells you just how complex and time-consuming this can be if you're not prepared.

Think of your financial statements as the official language you use to communicate with the IRS, state agencies, and potential investors. Speaking this language fluently and accurately builds credibility and ensures you stay compliant from day one.

A rock-solid financial operation stateside gives you the clarity to make smart, strategic moves. It all begins with getting the fundamentals right, like securing your Employer Identification Number (EIN). If you haven't done that yet, check out our guide on how to get an EIN number for UK founders.

Think of this guide as your starting point. We'll help you turn a potentially daunting task into a genuine strategic advantage, so you can get back to what you do best: growing your business.

The Three Core US Financial Statements at a Glance

Every US company, regardless of size, needs to be familiar with these three key financial statements. Each one tells a different part of your company's financial story.

Statement | What It Shows | Key Components |

|---|---|---|

Income Statement | Your company's profitability over a specific period (e.g., a month or quarter). | Revenue, Cost of Goods Sold (COGS), Operating Expenses, Net Income/Loss. |

Balance Sheet | A snapshot of your company's financial position at a single point in time. | Assets (what you own), Liabilities (what you owe), and Equity (the difference). |

Statement of Cash Flows | How cash has moved in and out of your business from operations, investing, and financing activities. | Operating Cash Flow, Investing Cash Flow, Financing Cash Flow, Net Change in Cash. |

Together, these documents give you, your investors, and government agencies a comprehensive view of your company's financial health and performance.

Building Your US Accounting Foundation

Before you can even think about pulling financial statements, you need a solid system to capture the data in the first place. I often tell founders to think of their accounting software as the foundation of a house. If it’s built on shaky ground—or worse, configured for the wrong country—everything you build on top of it will be unstable.

Getting this right from day one is non-negotiable for US compliance. For UK founders, the natural temptation is to just replicate what you know. But setting up your US entity’s QuickBooks or Xero account demands a distinctly American approach. It’s about much more than just flicking a switch from GBP to USD; it’s about structuring your financial DNA to meet US standards from the get-go. This is where accuracy is born or where critical errors take root.

Start with a US GAAP Chart of Accounts

Your first and most important job is to establish a US GAAP-compliant Chart of Accounts. This is the skeleton of your entire financial reporting system, and it organizes every single transaction into the correct bucket. Simply using a default UK or IFRS template is one of the most common mistakes I see, and it creates massive headaches down the line.

A proper US chart of accounts has specific categorizations that might seem unfamiliar but are absolutely essential for your IRS filings. For example, it correctly structures equity accounts for a US C-Corp (think Common Stock and Additional Paid-In Capital) and includes expense categories unique to operating Stateside.

Registered Agent Fees: This is a recurring, US-specific compliance cost that needs its own line.

State Franchise Taxes: Unlike UK corporation tax, these are state-level taxes that must be tracked separately for reporting.

US Payroll Expenses: This bucket needs to be broken down into federal and state liabilities like FICA, FUTA, and SUI taxes, which have no direct UK equivalent.

Nailing this structure ensures that when you run reports, the numbers are already organized for your US tax preparer and investors who expect a standard American format.

Configure Multi-Currency and Bank Feeds Correctly

As a UK founder, you're going to be living in two currencies. Activating multi-currency features in your accounting software is a must, but the setup is what really matters. Your US company’s base currency must be set to USD. All your official reporting will be done in US dollars, period.

When your UK parent company injects that initial seed capital, that transaction needs to be handled carefully. It isn't just a simple transfer; it’s recorded as a contribution to equity on the US balance sheet, with the currency conversion locked in at the spot rate on the day of the transaction. Any fluctuation in the exchange rate between that day and your reporting date creates a foreign currency gain or loss that has to be accounted for.

A seamless setup involves connecting your US bank account directly to your accounting software via bank feeds. This automates the import of transactions, drastically reducing manual entry and the risk of human error. It’s the single best way to ensure your data is clean and reconciled.

For a deeper dive into this crucial first step, our expert guide to opening a U.S. bank account online for non-residents provides essential insights. An accurate bank feed is the lifeblood of timely and reliable financial statements.

Recording Your First Key Transactions

Let's walk through a real-world scenario. Your UK holding company sends $50,000 to your new US Delaware C-Corp's bank account as startup capital.

Here is how you would correctly record this in your US QuickBooks or Xero:

Create a Journal Entry: You'll debit (increase) your US bank account by $50,000.

Credit Equity: At the same time, you'll credit (increase) an equity account, typically named "Additional Paid-In Capital" or "Shareholder Contribution," by $50,000.

This simple entry correctly establishes the financial relationship between the parent and the sub from a US GAAP perspective. It’s a clean record showing the business was funded by its owners, not through revenue or a loan. Creating this solid paper trail from day one makes preparing accurate financial statements infinitely more straightforward.

Mastering the Month-End Close Process

If there’s one secret weapon against year-end chaos and messy reporting, it’s a disciplined month-end close. For UK founders juggling a US entity, this monthly rhythm is about more than just ticking boxes—it's about creating a repeatable system that gives you a crystal-clear, real-time snapshot of your company’s financial health.

Think of it like this: waiting until December to sort out your financials is the business equivalent of cramming for a final exam the night before. You'll get it done, but it will be painful and probably full of errors. A monthly close, on the other hand, is like studying a little bit each week. It's manageable, far less stressful, and the results are infinitely better.

Gathering Your Source Documents

Every solid close process starts with gathering the raw data. This is your paper trail, the hard evidence that backs up every single number on your reports. For your US operation, this means corralling a specific set of documents, most of which will be in USD.

Your monthly document checklist should always include:

US Bank and Credit Card Statements: Make sure you download the official PDF statements for all your US-domiciled accounts. Don't just rely on the bank feed.

Invoices and Receipts: This includes all sales invoices sent to US customers and every receipt for expenses paid out of your US accounts.

Payroll Reports: If you have US staff, you’ll need the reports from your payroll provider (like Gusto or Rippling) that detail wages, taxes, and benefits.

Intercompany Records: It's vital to document any transactions between your UK and US entities, whether it's a loan, a management fee, or a shared expense.

A simple but game-changing habit is to create a centralized, digital folder for each month's documents. This keeps everything organized and ready for the most important phase: reconciliation.

Reconciliations: The Heart of Accuracy

With your documents in hand, the real work begins. Reconciliation is simply the process of matching the transactions in your accounting software, like Xero or QuickBooks, to your actual bank statements. It’s how you confirm that every dollar that came in or went out of your bank account is properly accounted for in your books.

This process is completely non-negotiable. Without a clean bank reconciliation, you simply cannot trust the numbers on your income statement or balance sheet. It is the single most important control for ensuring the integrity of your financial data.

Beyond the bank, you’ll need to reconcile other key accounts. This means matching your accounts receivable balance to your list of outstanding customer invoices and your accounts payable balance to unpaid supplier bills. One of the most common pain points I see with UK founders is the intercompany account, which tracks money owed between the UK parent and the US subsidiary. Reconciling this account every single month will save you from major headaches when it’s time for consolidated reporting.

Making Adjusting Journal Entries

The final step before you can confidently run your reports is to account for business activity that hasn't hit your bank account yet. We handle these through adjusting journal entries, and they are essential for preparing financial statements on an accrual basis, which is required by US GAAP.

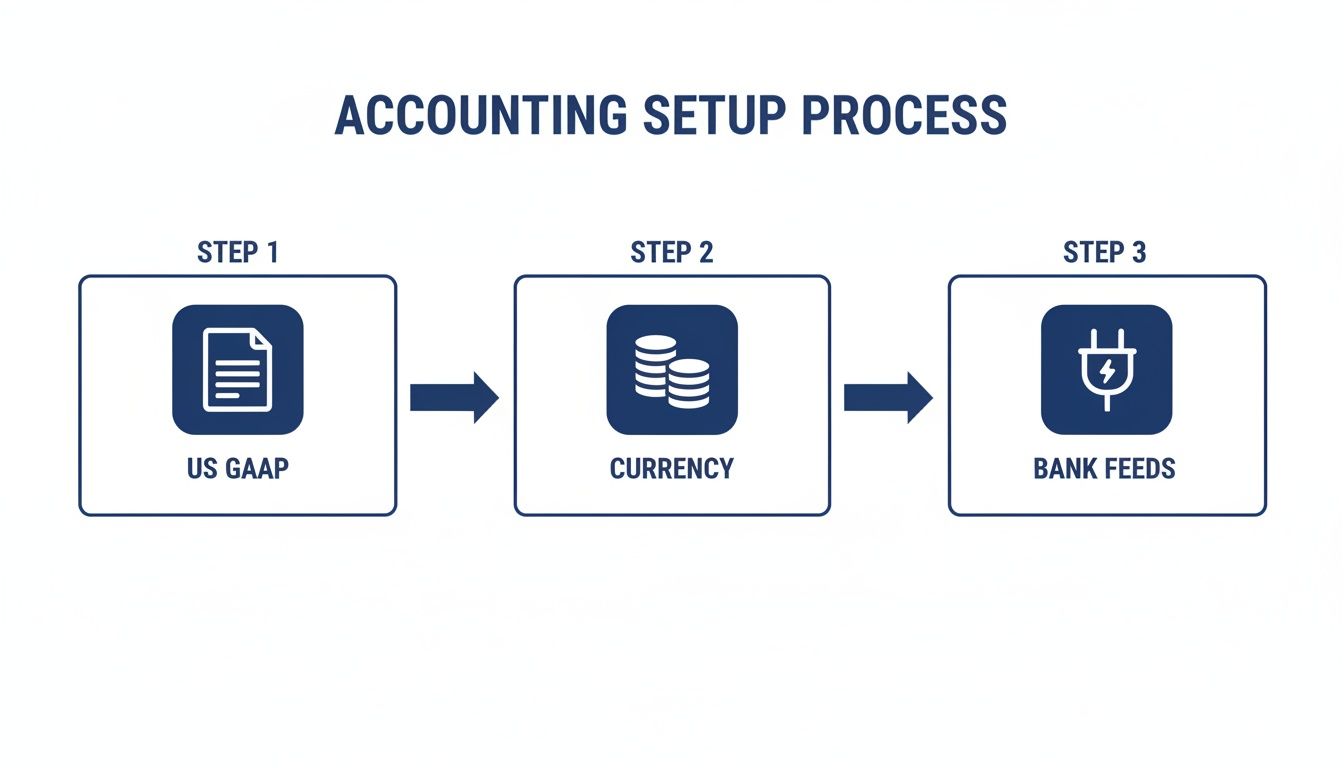

This infographic highlights the core elements—US GAAP principles, currency considerations, and automated bank feeds—that all feed into an efficient close process.

As the flow shows, a smooth month-end close really depends on getting the initial setup right, so you can trust the data coming in from the start.

Here are a few real-world scenarios where you’d need a journal entry:

Accrued Expenses: Imagine you got a $2,500 invoice from a US marketing contractor for work they did in March, but you aren’t scheduled to pay it until April. You need to record an entry in March to recognize that expense when it happened, not when the cash leaves your account.

Prepaid Expenses: Your company pays $1,200 in January for a 12-month software subscription. You can’t expense the whole amount in January. Instead, you'll post a journal entry each month to expense just $100, matching the cost to the period it benefits.

Sales Tax Payable: If you're collecting sales tax in a US state, you must calculate the total tax collected from customers and record it as a liability owed to the state. This isn’t your money—it’s just passing through.

By consistently gathering documents, performing reconciliations, and making these crucial adjustments, you build a financial record you can actually rely on. This disciplined monthly process is the only way to produce financial statements that are accurate, compliant, and genuinely useful for making smart decisions.

Navigating US GAAP and Currency Conversion

For many UK founders, this is where things get tricky. You've likely built your entire business around UK GAAP or IFRS, but your U.S. company has to play by a different rulebook: U.S. Generally Accepted Accounting Principles (GAAP).

These aren't just minor differences in terminology. They can genuinely change your reported profits and the value of your assets. On top of that, you're constantly juggling two currencies. Every dollar spent or earned needs to be recorded correctly, and then everything has to be translated back into pounds for your consolidated UK accounts. Getting a handle on both is non-negotiable for staying compliant on both sides of the pond.

Key Differences US GAAP vs UK GAAP/IFRS for Startups

While both sets of standards aim for the same goal—fair and accurate reporting—some specific differences often catch founders out. You don't need to be an expert on every nuance, but knowing the big ones is crucial. Misinterpreting these rules can lead to inaccurate financials, which is the last thing you want when dealing with the IRS or courting investors.

Here’s a quick look at the distinctions that matter most for growing companies.

Key Differences US GAAP vs UK GAAP/IFRS for Startups

This table breaks down some of the most common accounting treatments you'll encounter and how they differ between the U.S. and the UK.

Accounting Area | US GAAP Treatment | UK GAAP / IFRS Treatment |

|---|---|---|

Inventory Valuation | Allows the Last-In, First-Out (LIFO) method, where the most recently acquired inventory is sold first. | LIFO is strictly prohibited. Only First-In, First-Out (FIFO) or weighted-average cost methods are permitted. |

Development Costs | Research and development costs are almost always expensed as they are incurred, with very few exceptions. | Certain development costs can be capitalized as an intangible asset if specific criteria for future economic benefit are met. |

Revenue Recognition | Follows a detailed, five-step model under ASC 606, focusing on control transfer to determine when revenue is recognized. | IFRS 15 is very similar to ASC 606, but subtle differences in contract interpretation can lead to different timing. |

Lease Accounting | Leases are classified as either operating or finance leases, both of which are recorded on the balance sheet. | IFRS 16 has a single lease model, generally requiring all leases to be capitalized on the balance sheet. |

Think about it this way: a U.S. e-commerce company could use the LIFO method for its inventory. If costs are rising, this would result in a lower reported profit and, therefore, a lower tax bill. A UK company simply doesn't have that option. It's a clear example of how accounting rules can directly impact your bottom line.

Managing Currency Conversion and Translation

When you're running a business in both USD and GBP, you need a disciplined system for managing currency. Your U.S. entity’s books will be in U.S. dollars—that’s its functional currency. But you'll constantly have transactions and reporting needs that bridge both currencies.

Here’s how to approach it:

Record USD transactions on the day. Every transaction should be recorded in USD using the exchange rate for that specific day (the "spot rate"). Good accounting software like QuickBooks or Xero can automate this for transactions coming through a bank feed.

Track your foreign exchange gains and losses. Let's say you get an invoice in pounds but pay it a week later from your U.S. dollar bank account. The exchange rate will have shifted. That difference creates a realized foreign exchange gain or loss, which needs to be logged on your income statement. It’s a real P&L item.

Translate financials for consolidation. At the end of the month, quarter, or year, you'll need to translate the entire U.S. financial statement into GBP for your UK parent company’s reports. This isn't a simple currency swap. Assets and liabilities are translated at the closing rate, while income statement items are typically translated using an average rate for the period.

The constant movement between USD and GBP means you can't just set it and forget it. You have to actively manage your currency exposure and understand how translation affects your consolidated equity. A passive approach just won't cut it for accurate global reporting.

For UK tech companies with U.S. subsidiaries, getting this right is fundamental. Standards are always evolving, too. For instance, the Financial Accounting Standards Board's (FASB) ASU 2023-09 now requires more detailed income tax disclosures, a key detail when you're trying to navigate U.S.-UK tax treaties. You can dig into these kinds of financial reporting insights from PwC to stay on top of changes. Ultimately, building a clean and defensible financial record for your EIN-registered company is one of the most important things you can do.

Connecting Your Statements to Tax Filings

All that hard work preparing your financial statements isn't just an internal checkpoint. It's the critical first step in meeting your legal tax obligations in the United States. Think of your income statement and balance sheet as the official evidence you'll be submitting to the IRS and various state tax authorities.

For UK founders, this is where the rubber really meets the road. The numbers you've carefully compiled and reconciled throughout the year are put to their ultimate test. Accuracy is no longer just good business practice—it's a legal requirement.

From Net Income to Your Federal Tax Return

The most direct connection is between your income statement and your federal tax return. For a U.S. C Corporation, the main tax form you’ll deal with is Form 1120, U.S. Corporation Income Tax Return. The very starting point for this form is the net income (or loss) figure pulled straight from your income statement.

But it’s not a simple copy-and-paste job. Your book income, calculated under U.S. GAAP, needs to be reconciled with your taxable income. This means making a series of adjustments for items that accounting rules and tax laws treat differently.

Common adjustments you’ll likely encounter include:

Depreciation: Tax depreciation methods, like MACRS, often let you write off assets much faster than the straight-line method you probably use for your books.

Meals and Entertainment: The IRS has strict limits on how much of these expenses you can actually deduct, which are almost always tighter than what you've recorded.

Accrued Expenses: Some expenses you've recorded on an accrual basis might not be deductible for tax purposes until you’ve actually paid the cash.

This whole reconciliation process is formally documented on Schedule M-1 or M-3 of Form 1120. It creates a clear, auditable trail from your financial statements to the final tax bill you report to the IRS.

State-Level Compliance and Filing Obligations

Beyond the federal government, your financial statements are absolutely essential for handling state-level obligations, which can get surprisingly complicated. Each state has its own set of rules, creating a compliance web that founders have to navigate carefully.

For instance, many states levy a franchise tax, which is basically a fee for the privilege of doing business there. This tax might be based on your net worth (from the balance sheet), gross receipts (from the income statement), or some other formula. Delaware, a hugely popular state for incorporating, calculates its franchise tax based on the number of authorized shares or a complex alternative method involving your gross assets.

Your financial statements become the single source of truth for a wide range of state filings. Without accurate, up-to-date reports, you risk miscalculating taxes, incurring penalties, and falling out of good standing with state authorities.

On top of that, most states require you to file an annual report to keep your company's information current. These reports often ask for key financial data, like total assets or annual revenue, which you'll source directly from your statements. Keeping track of all these varied deadlines and requirements is crucial for maintaining your company's legal status in every state where you operate. Understanding how to calculate estimated tax payments for your U.S. business is another key piece of this puzzle.

Ultimately, the journey from daily bookkeeping to a successfully filed tax return is paved with the data from your financial statements. For UK founders, a dual US-UK tax expert can be an invaluable partner in this process, making sure every number is correctly reported and optimized for compliance on both sides of the Atlantic.

When to Bring in an Accounting Expert

As a founder, your time is your most valuable commodity. It's one thing to understand the basics of preparing financial statements, but it's another thing entirely to execute them flawlessly while you're also trying to scale a business. At some point, the DIY approach just doesn't scale, and knowing when to call for backup is crucial for your company's financial health.

Let's be honest, founders are stretched thin. A recent study revealed that a staggering 40% of CFOs aren't fully confident in their own financial data. Think about that for a second. If seasoned finance chiefs are worried, imagine the risk when you're also the CEO, head of sales, and lead product visionary. This isn't just about offloading a task; it's about gaining the clarity and confidence you need to make smart decisions.

Tipping Points: When to Get Professional Help

Certain moments in your company's journey are clear signals that it's time to bring in a professional. These aren't signs of weakness—they're signs of success. Your business is growing up, and your financial management needs to mature with it.

Keep an eye out for these key triggers:

You've Hired Your First US Employee: The moment you do this, you're thrown into the deep end of US payroll. You'll be dealing with federal and state tax withholdings like FICA and SUI, which are a world away from the UK's PAYE system.

You're Expanding into Another State: Every state is its own beast with unique tax laws. Once you hit a certain sales or activity threshold, you establish "nexus," which means you're on the hook for collecting and remitting sales tax. It's a compliance minefield you don't want to navigate alone.

You're Raising Money from US Investors: American VCs and angel investors live and breathe US GAAP. If you show up to a pitch with anything less than perfect, GAAP-compliant financials, you risk looking unprofessional and could jeopardize the entire funding round.

Bookkeeping is Eating Your Week: If you're spending more than a couple of hours a month wrestling with reconciliations or chasing down receipts, that's a huge red flag. That's precious time you should be spending on your product, your customers, and your growth strategy.

The Real Value of a Dedicated Partner

Working with an expert partner like Set Up Stateside isn't just about outsourcing your bookkeeping. It's about entrusting your entire financial workflow to a team that gets it. We can handle everything from setting up your accounting software and running monthly reconciliations to preparing board-ready financial statements you can actually trust.

An expert accountant doesn't just record what happened; they help you understand why it happened and what to do next. They uncover the story hidden in your numbers, turning financial statements from a boring compliance task into a powerful tool for growth.

This kind of partnership completely changes the game. It turns your financial operations from a reactive headache into a proactive, strategic asset. You don’t just get accurate reports; you get a trusted advisor who understands the specific challenges a UK founder faces when building a business in the US.

Common Questions from UK Founders

Making the leap across the pond brings up a ton of questions, especially when you're used to UK accounting rules. We've worked with hundreds of UK founders setting up their U.S. operations, and a few key questions always come up. Here’s what you need to know about preparing financial statements for your U.S. entity.

How Often Should I Prepare Financial Statements?

Technically, you only need to produce them once a year for your U.S. tax filings. But I can't stress this enough: that is a terrible idea.

The best-run companies close their books and prepare a full set of financial statements every single month. Think of it as taking a real-time pulse of your business. It helps you make smarter, faster decisions on everything from hiring your next engineer to adjusting your marketing spend.

Plus, you’ll always be ready for that unexpected investor update or due diligence request. A consistent monthly close makes the year-end process a simple review, not a frantic scramble to figure out what happened last March.

Can I Use My UK Accounting Software?

Please don't. This is a critical—and surprisingly common—misstep. You absolutely must set up a separate, U.S.-based subscription for your accounting software, whether you're using QuickBooks Online or Xero.

This is about more than just switching the currency from GBP to USD. A U.S. account configures your entire system for American compliance from day one.

The Chart of Accounts will be structured for U.S. GAAP, not UK GAAP or IFRS.

Tax settings are built to handle IRS and state-level requirements, which are wildly different from HMRC.

Reporting formats will match what U.S. investors, banks, and CPAs expect to see.

Trying to run a U.S. company out of a UK software instance creates a tangled mess of compliance issues. Trust me, it’s a nightmare to unravel later, and it's always an expensive fix.

The single biggest mistake we see is founders applying UK accounting logic to their U.S. books. From miscategorizing intercompany loans to forgetting about state-specific liabilities like sales tax, these errors can compound quickly and create significant compliance risks by year-end.

What Are the Biggest Mistakes UK Founders Make?

Aside from the software issue, a few other pitfalls regularly trip up founders. The most common one is mixing personal and business expenses—it seems small, but it can get you into hot water fast. We also frequently see capital injections from the UK parent company recorded incorrectly.

Another big one? Simply failing to perform monthly bank reconciliations. A small discrepancy that you ignore in March can snowball into a massive, untraceable problem by December. It’s the foundational discipline of good bookkeeping.

Do I Need an Audit for My Financial Statements?

For the vast majority of startups, the answer is a firm no. A formal, independent audit is an intense and expensive process. It’s usually only necessary when you're raising a major funding round from VCs (think Series A or B), gearing up for an IPO, or if a major lender demands one as part of a loan agreement.

But just because you don't need an audit doesn't mean you can be sloppy. Your statements still must be accurate and prepared according to U.S. GAAP. These aren't just for you; they are the official financial records that form the basis of your legal tax filings with the IRS and state agencies.

Navigating these complexities is what Set Up Stateside does best. We provide the expert accounting and tax support you need to stay compliant and focused on growth. Learn more about our services.

Comments